Examples of hard credit inquiries

A lender may perform a hard inquiry when you apply for a new loan or line of credit, such as a credit card, personal loan, mortgage, car loan or student loan. Landlords sometimes may perform a hard credit pull when you apply to rent a home.

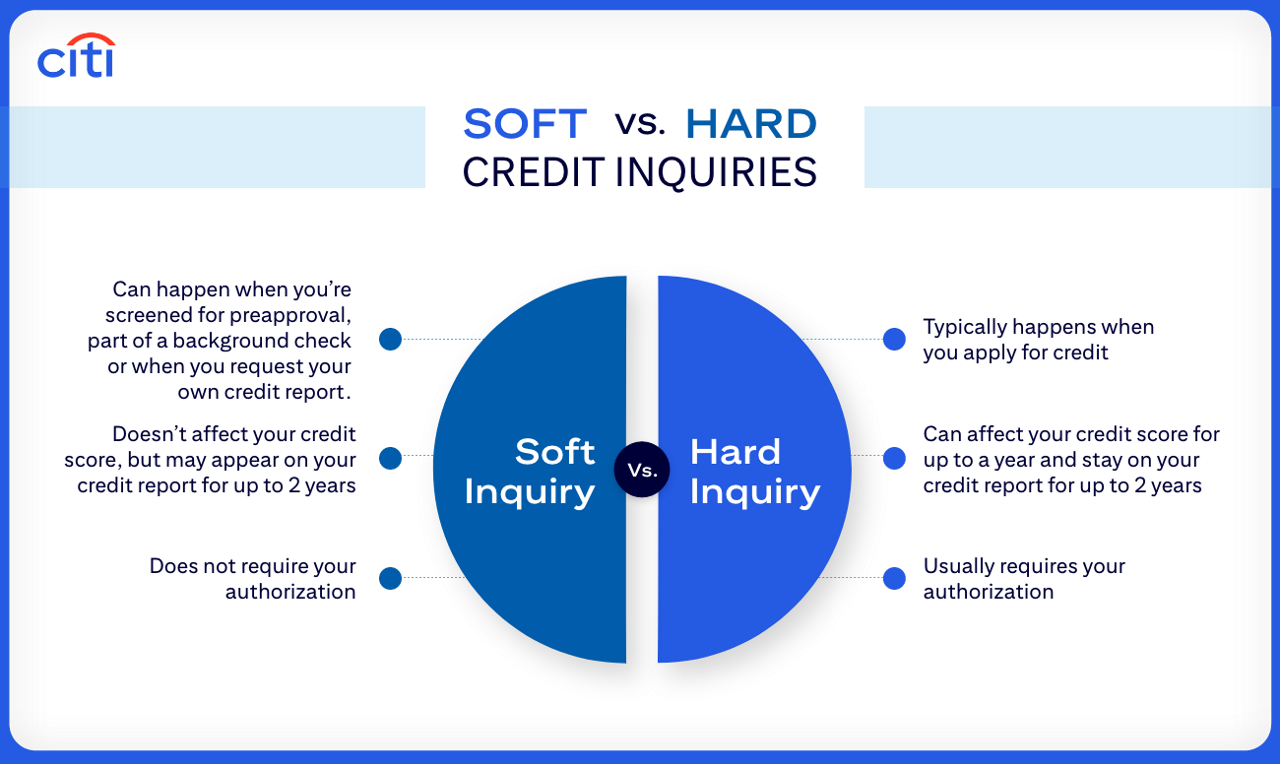

What is a soft credit inquiry?

Soft credit inquiries – sometimes called “soft credit checks” or “soft pulls” – may happen when you’re screened for preapproval, as part of a background check or when you ask for a copy of your own credit report. Unlike hard inquiries, soft inquiries can happen even if you didn’t authorize them or apply for a loan or line of credit.

How does a soft credit inquiry affect your credit?

Soft credit inquiries do not affect your credit score. Only you can see soft inquiries when you check your own credit. They typically stay on your credit report for a year or two.

Examples of soft credit inquiries

Some examples of soft credit inquiries include when you check your own credit, when a lender checks your credit to prequalify you for an offer and when an employer checks your credit as part of an employment screening process. Your current creditors may also perform soft pulls periodically.

Unauthorized or unfamiliar inquiries

Understanding the difference between soft and hard credit pulls can help you better evaluate your credit report for errors and fraud.

You can request one credit report from each of the three major credit bureaus every twelve months. When reviewing your credit report, you may see unfamiliar soft pulls – remember, lenders can check your credit for preapproval offers, and your existing creditors may occasionally check your credit. Keep an eye out for unauthorized hard inquiries – these can be signs of fraud or mistakes.

If you see an unauthorized hard inquiry, you can dispute it with the credit bureau. It can also be a good idea to contact the institution that performed the inquiry. If you suspect you’re a victim of fraud, you can freeze your credit or place a fraud alert on your credit.

Disclosure: This article is for educational purposes. It is not intended to provide legal, investment, or financial advice and is not a substitute for professional advice. It does not indicate the availability of any Citi product or service. For advice about your specific circumstances, you should consult a qualified professional.